Hey — Max here 💪

Before we dive in, let me say a few words.

What you’re about to read is the kind of research we typically reserve for our Premium work — high‑conviction, step‑by‑step analysis built for dividend investors who prioritize staying power over headlines. The goal is simple: find businesses that can compound dividends over long periods, avoid “high yield, low quality” traps, and build an income stream that doesn’t fall apart when the market gets chaotic.

This is process‑driven, cycle‑aware investing. Not a one‑quarter trade thesis, but a repeatable framework designed to hold up through recessions, inflation bursts, rate shocks, commodity swings, and rotating market leadership. Today you’re getting a full taste of that approach. In future issues, we’ll surface additional dividend ideas and less obvious opportunities — companies with the operational DNA to become the next generation of durable dividend growers.

The edge isn’t complicated: identify quality before it becomes consensus, and execute with a plan. Instead of buying after the story is widely celebrated, you aim to position yourself early — with clear expectations for income, downside risk, and long‑run compounding.

When investors think about what’s truly “essential” to the real economy, it’s not just utilities or consumer staples. The economy also runs on physical work: building roads, expanding data centers, moving materials, extracting energy, and repairing infrastructure. None of that happens without heavy equipment — and that’s what makes Caterpillar (CAT) a textbook company to study for dividend investors.

Caterpillar is one of the world’s leading manufacturers of construction and mining equipment, diesel and natural gas engines, industrial turbines, and locomotives — supported by a dealer network that functions like a global service-and-parts distribution machine. CAT isn’t a “story stock.” It’s an operational business tied to real capital spending, real projects, and real replacement cycles. And yes — it’s cyclical. End markets like construction, mining, and energy can slow hard when conditions tighten.

But Caterpillar’s model has qualities dividend investors should respect. The installed base creates a long runway for parts and service revenue, dealers provide reach and responsiveness that’s difficult to replicate, and scale supports manufacturing efficiency and purchasing power. When run with discipline, that combination can turn a cyclical equipment maker into something closer to a cash‑generation engine across a full cycle — not every quarter, but over time.

That distinction matters. Many cyclical industrials look “cheap” at the top of the cycle and “expensive” at the bottom. For dividend investors, the question isn’t whether CAT can produce strong results in good years — it clearly can. The question is whether the company has the balance sheet, operating discipline, and capital allocation framework to keep paying (and ideally growing) dividends when demand cools, inventories rise, or credit conditions tighten.

Caterpillar has built a shareholder‑friendly reputation over decades, with the dividend as a core commitment rather than an afterthought. The key issue is whether that payout is supported by durable free cash flow and sensible reinvestment — not by timing, leverage, or a temporary boom in end markets.

So the real question isn’t whether Caterpillar is a “good company.”

The question is:

Does Caterpillar fit your plan right now — at today’s valuation, yield, and realistic dividend growth outlook — or is it better treated as a watchlist name until the setup becomes more attractive?

In this Deep Dive, Caterpillar goes through the MaxDividends Five‑Pillar Formula — the same practical checklist we use to identify companies that can keep paying (and growing) dividends through recessions, cost inflation, and market volatility.

Love what we’re building? Our Founding Partners already enjoy lifetime access to premium content, the app, and our community. Thank you for being a part of it!

👉 Let’s break it down — step by step.

Table of Contents

How This Company Makes Money?

Do I clearly understand how Caterpillar (CAT) earns its money — and does the business make sense?

CAT designs and manufactures heavy equipment and engines, but the real compounding machine is the combination of (1) a massive installed base in the field and (2) a global independent dealer network that sells, services, repairs, finances, and supplies parts over decades. Cash flow is driven by equipment demand across construction/resource/energy cycles plus the high‑value aftermarket stream that comes from keeping machines running — not by consumer branding, advertising spend, or rapid product-fashion cycles.

1️⃣ Equipment Leadership + Installed Base (The Cycle Engine)

But CAT’s edge is that each sale expands the installed base. Over time, that installed base becomes a durable economic asset: machines need maintenance, rebuilds, wear parts, and periodic replacement. In good years, original equipment volume lifts results. In softer years, the installed base helps cushion profitability because the fleet still needs to run.

2️⃣ Dealer Network (Distribution, Service, and Local Moats)

Caterpillar’s dealer network is not just a sales channel — it’s a competitive moat. Dealers provide local inventory, field service technicians, rebuild capabilities, parts availability, and customer relationships that are hard for competitors to replicate at global scale. For dividend investors, this matters because dealers help CAT stay close to end demand, manage aftermarket capture, and protect share even when customers become price‑sensitive. It also improves resilience: when markets slow, service work and parts logistics remain active because downtime is expensive for customers.

3️⃣ Parts & Service / Aftermarket (Margin and Cash Flow Quality)

In heavy equipment, the “razor-and-blades” dynamic is real. Aftermarket parts and service typically carry stronger margins and steadier demand than new equipment sales, because maintenance is non‑optional for customers running fleets in construction sites, mines, and energy operations. This is one reason Caterpillar can be a dividend investor’s cyclical: you’re not underwriting only the next equipment cycle — you’re underwriting a long stream of repair, replacement, and rebuild activity tied to the installed base. Higher aftermarket penetration also tends to increase customer stickiness: once service systems, parts catalogs, and technician relationships are embedded, switching costs rise.

4️⃣ Operational Discipline + Capital Allocation (The Compounding Mechanism)

Caterpillar doesn’t compound like a high-growth tech firm. Its long‑term compounding mechanism is industrial: pricing discipline, leaner production, tighter inventory management, continuous cost improvement, and thoughtful capacity decisions — while continuing to invest in product reliability and dealer support.

The key strength is that Caterpillar operates in the physical backbone of the economy: infrastructure, housing, mining, energy, and transportation. Those end markets are cyclical — but they don’t disappear. Machines still break, fleets still age, and projects still need to be finished. That doesn’t make CAT recession‑proof, but it does make the business model easier to underwrite than many high-yield setups that depend on permanently favorable conditions.

It’s not a black box. It’s an installed-base-and-service ecosystem built to win through uptime, dealer reach, and lifetime customer economics — the kind of structure that can support a long dividend record when paired with conservative financial management.

👉 And yes — this business model is clear, resilient, and makes perfect sense.

Is This a Good Stock to Buy Long Term?

Has the company shown the kind of consistency and resilience a long‑term dividend strategy needs?

Our approach is simple, but it works: we focus on businesses that can generate repeatable cash flow through an entire cycle and translate that cash into reliable, growing dividends. With a company like Caterpillar, the goal isn’t to pretend the business is “non‑cyclical.” It’s to own a cycle-tested industrial that has the tools to endure downturns: a massive installed base that sustains parts and service demand, a dealer network that keeps customers supported locally, and operating discipline that prioritizes cash generation over chasing volume at any cost.

The MaxDividends Strategy Checklist – Simple Steps to Pick the Right Stocks

Step 1: Dividend History

Our filter: Companies with 15+ years of consistent dividend growth.

Caterpillar doesn’t just “qualify” on dividend consistency — it shows the exact stair‑step pattern long‑term dividend investors want, especially impressive given how cyclical its end markets can be. CAT’s annual dividend per share rises from $1.8 in the early 2010s to about $5.80+ most recently. The progression is broadly upward with no visible dividend reset — just steady increases over time. That shape matters because it signals a payout backed by through‑the‑cycle cash generation and a management culture that treats the dividend as a non‑negotiable commitment, not a “nice to have” during boom years.

For a heavy equipment manufacturer tied to construction, mining, and energy cycles, that consistency is not automatic. It suggests Caterpillar has been able to produce enough free cash flow across very different environments and manage the balance sheet conservatively enough to avoid panic decisions. This is what a real industrial income compounder looks like in practice: not a gimmicky headline yield, not a one‑time special dividend story — but a methodical pattern of annual raises that reflects long‑term capital allocation discipline.

✅ Step 1 passed — Caterpillar (CAT) behaves like a Dividend Eagle, with a durable record of dividend increases that holds up despite cyclical demand and supports the case for CAT as a serious dividend-growth candidate.

Step 2: The Five-Pillar Secret Formula

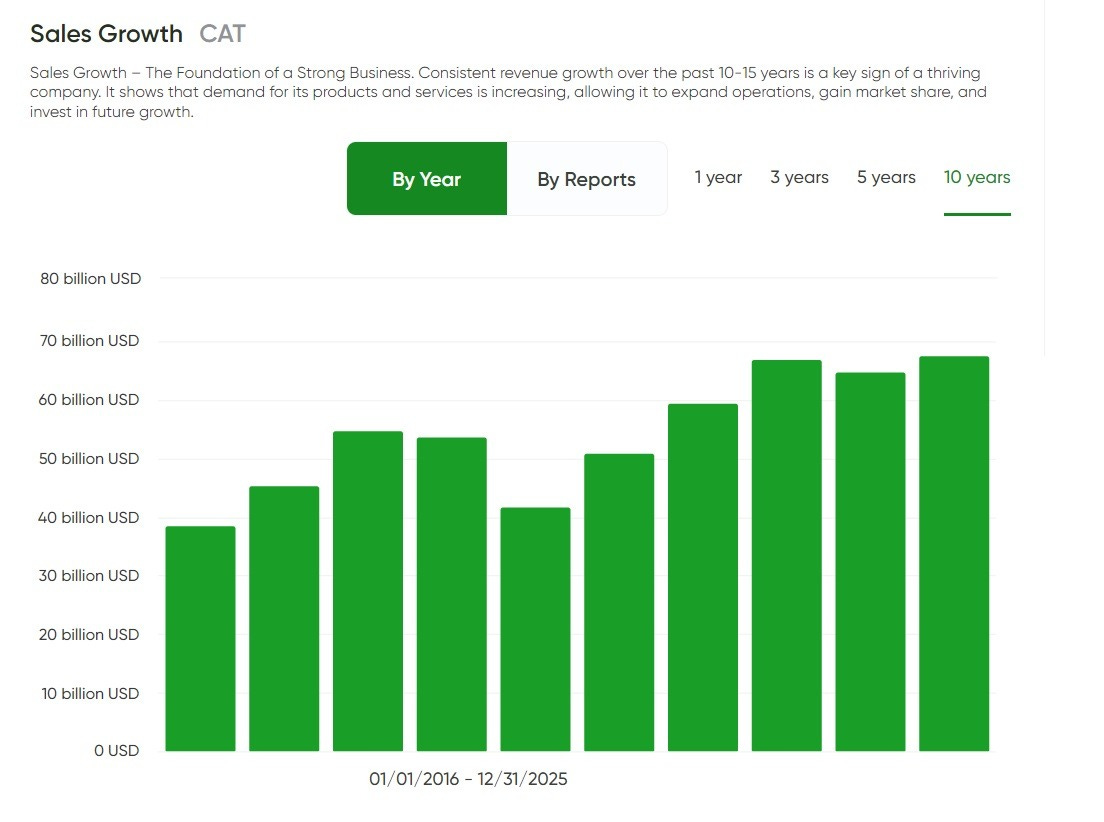

1️⃣ Sales Growth – The Foundation of a Strong Business

On the 10‑year view, Caterpillar’s sales grow from roughly ~$38B in the mid‑2010s to about ~$67B most recently. The path isn’t a straight line — and it shouldn’t be. CAT is tied to construction activity, mining capex, energy investment, and broader credit conditions. But the long‑term direction is clearly higher.

That pattern fits the reality of Caterpillar’s business model. CAT doesn’t grow because of consumer “discovery” or marketing-driven demand. It grows when the installed base expands, customers invest in fleet renewal, and the company captures more lifetime value through parts, service, rebuilds, and technology-enabled productivity upgrades. Over time, that ecosystem can lift revenue even if any single year is choppy.

The dip in the middle of the decade-long picture is the kind of stress test dividend investors should actually want to see. It highlights the cyclicality — conditions tighten, projects slow, and equipment demand cools. The more important point is what happens next: the rebound back to a higher revenue run-rate suggests the franchise is durable and that end-market recoveries translate into real sales power.

For an income investor, that recovery characteristic matters almost as much as the growth itself. It supports the case that Caterpillar can keep generating enough cash through the cycle to defend — and over time grow — the dividend.

✅ Sales Growth passed — Caterpillar’s higher long-term revenue base, despite cyclical drawdowns, supports the view of CAT as a durable industrial platform with a credible foundation for dividend growth.

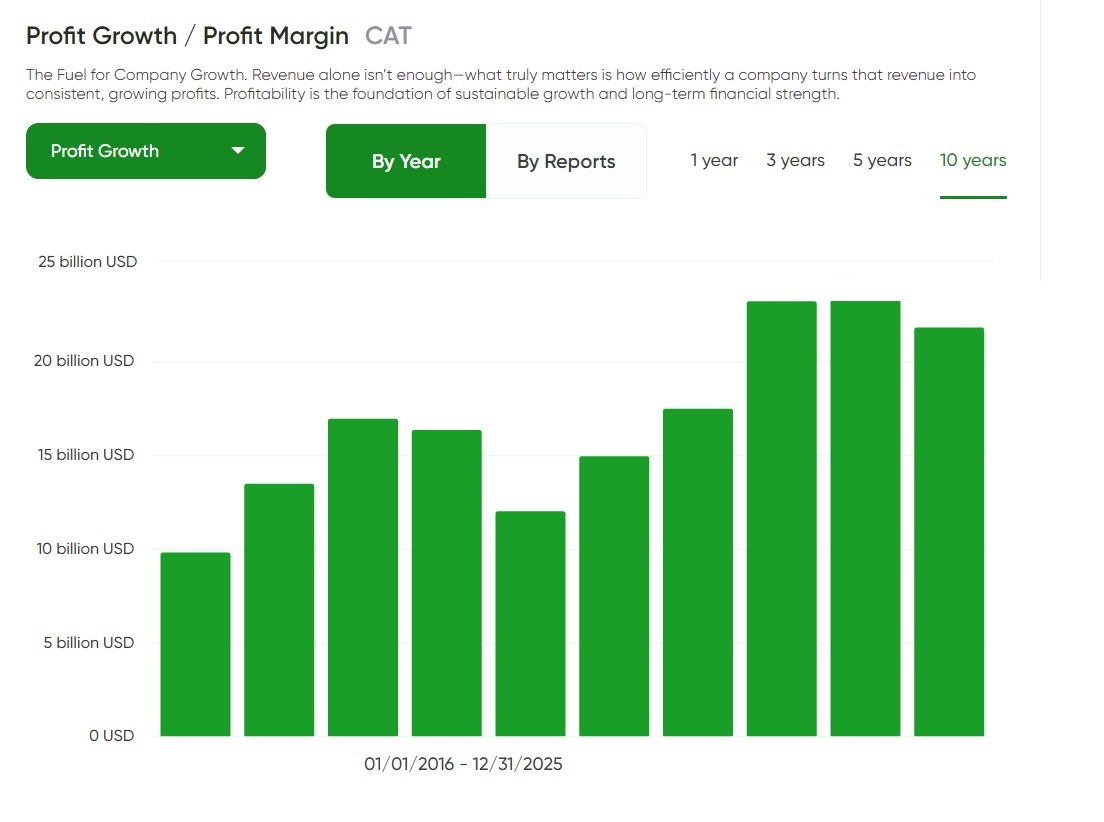

2️⃣ Profit Growth – The Fuel for Dividend Growth

Caterpillar’s profit growth reinforces the same message as the revenue trend — but with an added layer of confidence: profitability has expanded over time in a way that looks structural, not like a one‑off peak. Over the last decade, profits rise from roughly ~$10B to the low‑$21B range most recently, with a noticeable step up after the softer middle years and continued strength into the latest period. For a cyclical industrial, that matters. It suggests Caterpillar isn’t simply benefiting from a temporary burst of demand, but operating from a higher earnings base than it did in prior parts of the cycle.

The “why” matters, because this isn’t a story about Caterpillar suddenly finding a trendy growth pocket. In heavy equipment, the compounding mechanism is operational and installed‑base driven. When pricing and mix are managed well, earnings can expand even if unit volumes don’t grow perfectly. When the installed base grows, parts and service activity tends to rise alongside it, improving the quality and persistence of profits. And when cost discipline and productivity initiatives are executed consistently, incremental improvements can translate into meaningful progress in profitability over time.

What’s especially encouraging in the trend is the lack of a single, isolated spike that would suggest unsustainable conditions. Instead, it reads like a company that absorbed a difficult stretch, rebuilt momentum, and is now operating from a stronger profit foundation. For dividend investors, that’s the key point: a growing profit pool is what ultimately protects the payout, funds reinvestment in the dealer and service ecosystem, and supports the capacity for future dividend increases.

✅ Profit Growth passed — Caterpillar’s expanding profit base strengthens dividend durability and supports the case for continued dividend growth while preserving the financial flexibility needed to keep investing through the cycle.

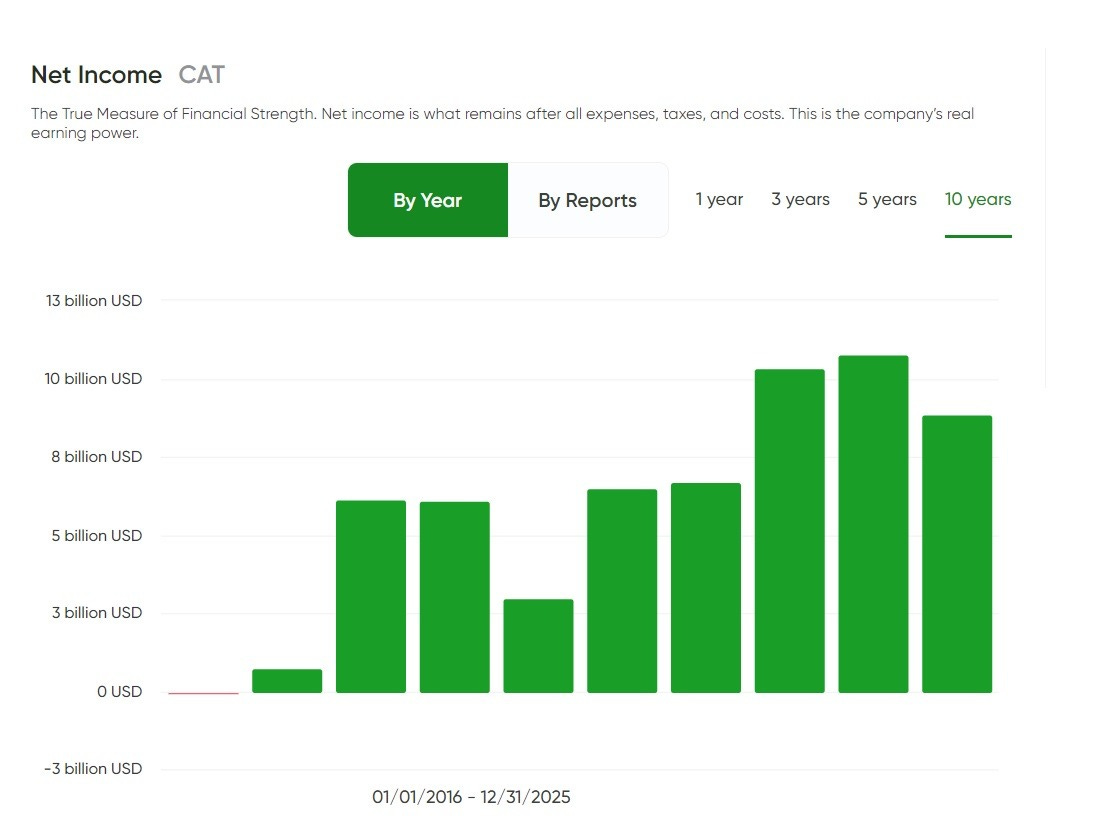

3️⃣ Net Income – True Measure of Strength

Caterpillar’s net income trend is a strong example of what dividend investors should look for: long‑term upward progress, with a visible “stress test” in the middle that proves the company can take a hit and still rebuild to a higher earnings base. Importantly, the decade begins with a loss, before earnings swing back into positive territory and expand materially. Over the 10‑year view, net income moves from that early negative result to roughly the $9–$11 billion range in the most recent years. The profile also includes a sharp drop in the middle of the period, followed by a steady recovery and then a move to new highs, with the latest year still elevated even if it comes off the absolute peak.

That pattern is exactly why we focus on direction and durability rather than demanding a perfectly smooth line. Caterpillar operates in highly cyclical end markets, so downturns can temporarily compress equipment demand and profitability. What matters for dividend compounding is whether the business can restore earning power when conditions normalize, and whether the post‑recovery baseline ends up meaningfully higher than the pre‑downturn level. In Caterpillar’s case, the answer appears to be yes: the earnings floor has moved up across the decade despite starting from an unusually weak point.

✅ Net Income passed — Caterpillar demonstrates a higher underlying earnings profile over the decade, reinforcing that its dividend growth is supported by real operating resilience rather than a temporary tailwind.

4️⃣ Dividend Payout Safety – Protecting Passive Income

For Caterpillar, the payout ratio story is a clear example of why dividend investors need to interpret this metric in context, not as a standalone “green/red” signal. For most of the period, CAT’s payout ratio sits in a relatively normal band that looks reasonable for a mature industrial that prioritizes returning capital to shareholders. Then you see the outlier: an extreme spike to roughly the high‑two‑thousands percent range, followed by another elevated reading in the low‑hundreds percent range, before the payout ratio settles back into a more typical zone afterward.

The reason matters, because this isn’t automatically what a structurally unsafe dividend looks like. It’s what happens when earnings temporarily collapse (or flip negative) while management chooses to keep the dividend intact. In Caterpillar’s case, the abnormal payout ratio spike reflects a period where reported net income was unusually depressed, so the dividend — which did not collapse alongside earnings — became enormous relative to the earnings base. In plain terms, the ratio blew out not because the dividend suddenly became reckless, but because the denominator briefly broke.

What dividend investors should focus on is what came next. The payout ratio normalizes back into a sustainable range, which suggests earnings power recovered and dividend coverage improved. That’s an important signal in a cyclical business: it indicates Caterpillar treated the dividend as a long-term commitment through a weak patch, and once conditions stabilized, the company generated enough profit again to support the payout without permanently living on the edge.

✅ Dividend Payout Safety passed — despite a temporary distortion during an earnings shock, Caterpillar’s payout ratio has returned to a more sustainable range, supporting the view that the dividend is affordable under normal conditions and can continue compounding without cornering the balance sheet.

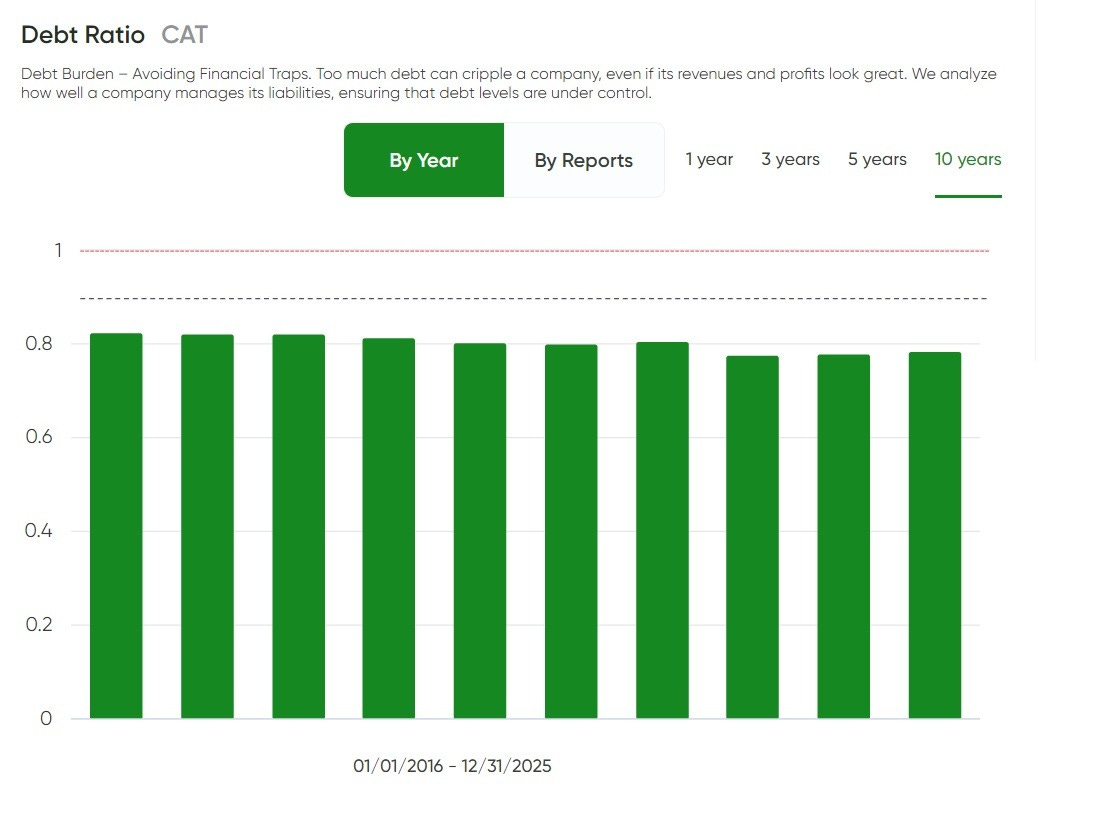

5️⃣ Debt Burden – Avoiding Financial Traps

Caterpillar does use debt, and that shouldn’t automatically scare dividend investors off. Heavy equipment manufacturing is capital-intensive, and CAT also operates a sizable financing arm that supports dealer and customer purchases. The real question isn’t whether leverage exists, but whether it’s controlled and stable — or whether it’s creeping higher in a way that eventually forces uncomfortable tradeoffs between reinvestment, buybacks, and the dividend.

On the 10‑year debt ratio view, Caterpillar’s leverage looks elevated but managed. The ratio sits in a fairly tight range around the ~0.78–0.82 area for most of the period, with a modest improvement later on rather than a steady march upward. That’s what “managed leverage” tends to look like in a mature industrial: not debt‑free and not ultra‑conservative, but also not showing the kind of balance‑sheet deterioration that usually precedes dividend stress.

✅ Debt burden passed — leverage is high, but Caterpillar’s pattern looks more like structural leverage supporting a capital‑intensive model, with the key positive being the overall stability of the ratio across the cycle.

Bottom Line: The Company Financial Condition?

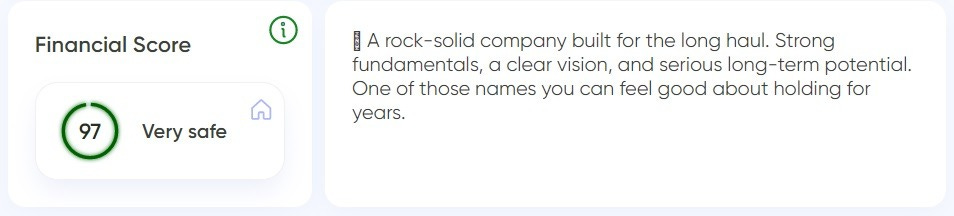

Financial Score 90+ ✅

For Caterpillar (CAT), the Financial Score comes in at 97 (“Very safe”). That clears our 90+ threshold comfortably and signals a financial profile that’s built for durability — exactly what dividend investors want when the plan is to hold through multiple economic environments, not just the next quarter. In practical terms, a score in this range supports the idea that Caterpillar has the financial resilience to operate through cyclicality in construction, mining, and energy markets, continue investing in its dealer and service ecosystem, and still protect the dividend strategy without being forced into reactive capital allocation decisions at the wrong point in the cycle.

MaxDividends Five-Pillar Secret Formula. Step 2 – ✅

Caterpillar (CAT) comes out of our Five‑Pillar review looking like the type of dividend stock you can realistically own through a full cycle — not just a name that works when conditions are perfect.

The dividend record is the first clue. Caterpillar’s payout history shows the stair‑step pattern long‑term income investors look for, reflecting a dividend that’s treated as a priority and raised methodically over time. The business fundamentals support that interpretation. Over a decade-long view, Caterpillar operates from a meaningfully larger revenue base than it did in the mid‑2010s, and its earnings power ultimately moved higher as well — even though the period begins from a notably weak point that included an early loss.

The “messy” part in the middle of the period is important, because it wasn’t random. Caterpillar’s results are tied to construction activity, mining investment, energy markets, and credit conditions, so downturns can hit equipment demand hard and compress profitability. The dividend investor takeaway isn’t that Caterpillar is immune to shocks — it’s that the company has demonstrated an ability to absorb a downcycle and still re‑establish earnings at a higher level afterward.

That also explains why the payout ratio can look distorted during the weak stretch. When earnings temporarily collapse or turn negative, even a steady dividend can screen as “unsafe” on a payout ratio chart because the denominator breaks. What matters is whether coverage improves when conditions normalize, and Caterpillar’s more recent payout levels suggest the dividend is again being funded by restored earnings power rather than by stretching indefinitely.

Leverage is part of Caterpillar’s model as well, especially given the capital intensity of the business and the presence of its financing operations, but the trend is what keeps it investable for conservative dividend strategies. The company carries meaningful debt, yet the leverage picture looks managed rather than progressively worsening, which reduces the odds of a future scenario where management is forced to choose between stabilizing the balance sheet and supporting the dividend.

Taken together, Caterpillar doesn’t just clear the checklist — it clears it with authority. A Financial Score of 97 places it firmly in our “very safe” tier and supports the view that CAT’s dividend profile is backed by durable operating capacity, with the downcycle stress test serving as evidence of resilience rather than a permanent scar.

✅ Passed: Caterpillar (CAT) — Proven Dividend Eagle.

Does It Fit My Plan?

Finding the Right Role for Every Dividend Stock – MaxRatio

Dividend stocks aren’t one-size-fits-all, and assuming they are is a common path to disappointment. The word “dividend” covers very different kinds of holdings: some are meant to be owned for decades as quiet compounders, others deserve a core slot because they pair income with reliable growth, and a smaller subset is mainly about generating the most cash right now.

That’s exactly what MaxRatio is for. It’s a straightforward way to map a dividend stock to its most logical job in a portfolio using three practical inputs: the current dividend yield, the pace of dividend growth, and the company’s overall financial strength. When you view those signals together, it becomes much clearer whether a stock belongs in a growth-leaning bucket, a balanced core allocation, or an income-first sleeve.

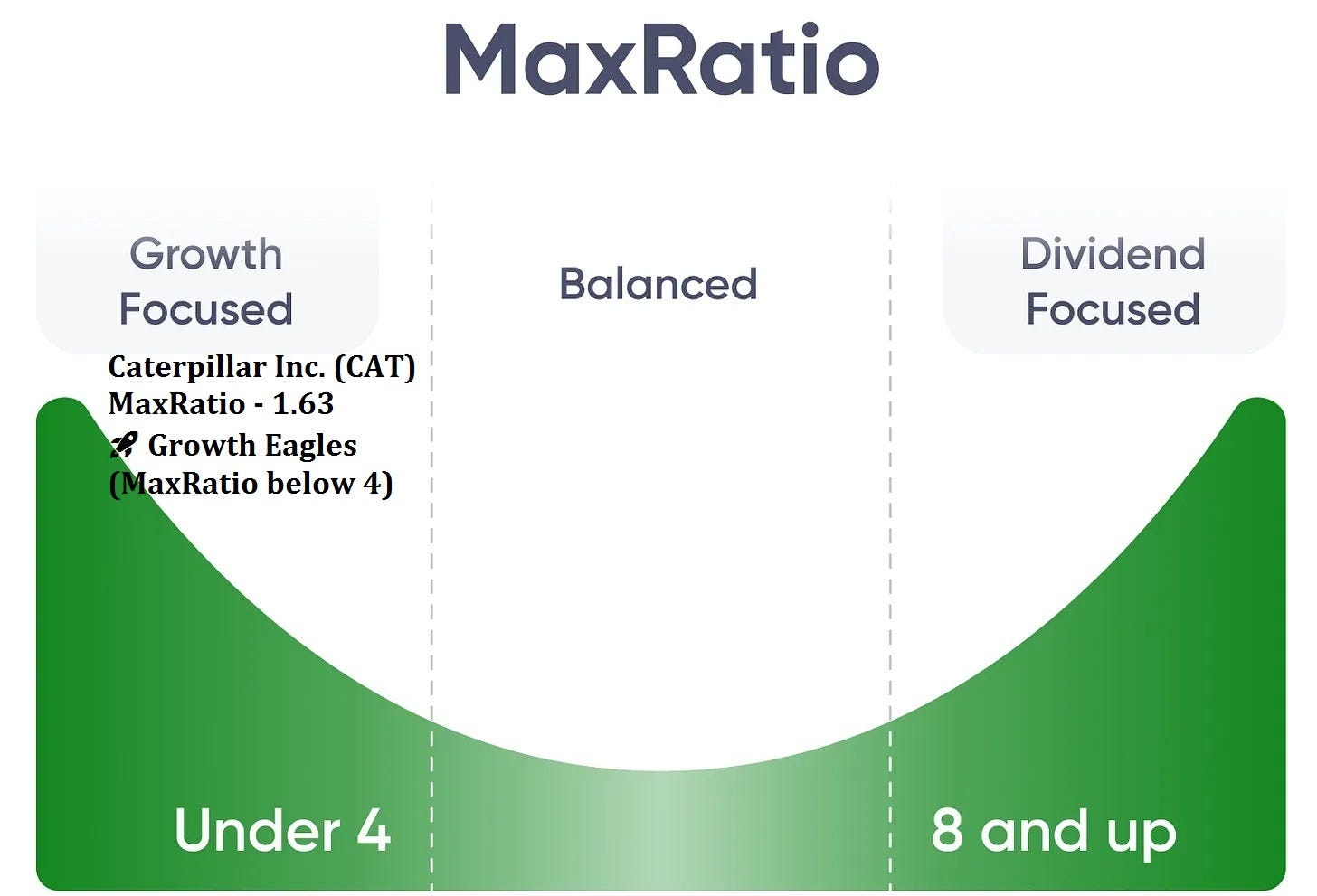

- 🚀 Growth Eagles (MaxRatio under 4) — are typically chosen for long-run compounding. The starting yield is often modest, but business quality and reinvestment capacity can translate into faster earnings and dividend growth over time.

- ⚖️ Balanced Eagles (MaxRatio 4–8) — often represent the “sweet spot” for many dividend investors. You get a respectable yield today, while dividend growth is usually strong enough to keep raising your income stream and support price appreciation through a full cycle.

- 💵 Income Eagles (MaxRatio 8+) — are primarily about near-term cash flow. They tend to offer higher yields upfront, but dividend growth is often slower, making them a better fit for investors who value current income more than maximizing long-term total return.

MaxRatio isn’t meant to label Caterpillar (CAT) as “good” or “bad.” It’s meant to answer the more practical question: what role should this stock play in a dividend portfolio? With Caterpillar, you’re generally looking at a company that emphasizes steady dividend progress and resilience rather than an attention-grabbing yield. It usually fits best as a core, plan-friendly holding for investors who want income that can grow over time without leaning on a fragile balance sheet.

Let’s Take Caterpillar (CAT)

Inside the MaxDividends app, you can open Company Analytics and, in seconds, pull the two numbers that matter most for quick dividend positioning: the Financial Score and MaxRatio. No spreadsheets, no jumping between tabs — just a clean read on quality and portfolio role.

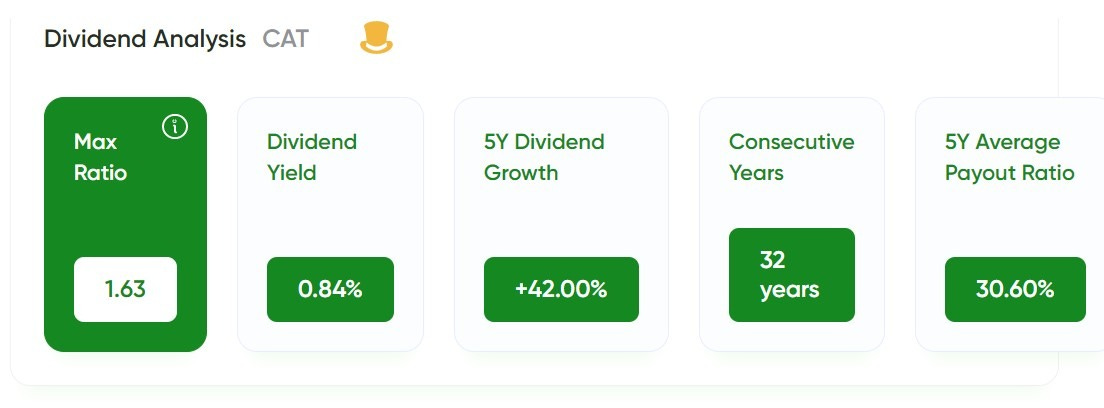

For Caterpillar (CAT), the MaxRatio snapshot lands decisively on the growth-leaning side of the framework. CAT shows a MaxRatio of 1.63, which places it in the Growth Eagles (MaxRatio below 4) category. In plain English, this is a dividend profile where the starting yield isn’t the headline feature, but the dividend growth engine has been powerful enough to drive long-run income compounding.

That positioning matches Caterpillar’s reality. With a dividend yield of roughly 0.84%, the stock clearly isn’t competing in the “highest yield” category. What stands out instead is dividend growth momentum, with +42.00% growth over the last five years, alongside a long record of commitment to shareholders reflected in 32 consecutive years of dividend payments.

The metric that keeps this from being a pure “set it and forget it” story is actually not the payout ratio. CAT’s 5-year average payout ratio of 30.60% looks conservative and leaves room for flexibility through the cycle. The real issue for dividend investors is different: Caterpillar is cyclical, so even with a disciplined payout policy, earnings can swing meaningfully when construction and resource markets cool. The takeaway is that CAT looks less like an income-heavy stock built to maximize cash today, and more like a long-duration dividend grower where income is designed to build over time — even if the ride isn’t perfectly smooth year to year.

For investors building a dividend portfolio with a long runway, Caterpillar’s role is clear. It’s not meant to be a high-yield anchor. It’s positioned as a compounding engine: a low starting yield, strong recent dividend growth, and a payout profile that looks affordable — giving the company room to keep raising the dividend across the cycle.

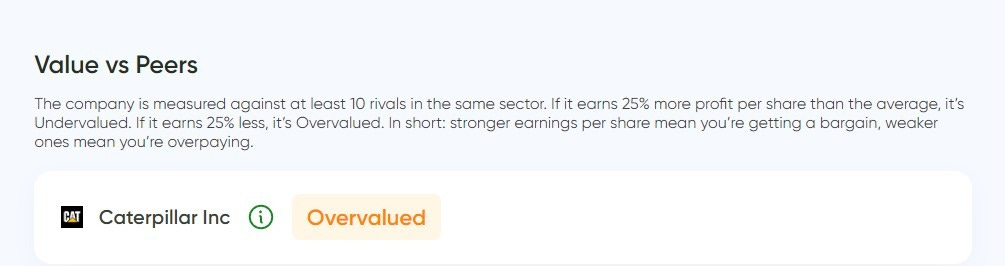

💵 Is the Stock Undervalued Today?

Cheaper than competitors?

⚠️ According to the MaxDividends App, Caterpillar (CAT) currently screens as Overvalued versus its peer group.

“Overvalued” doesn’t automatically mean Caterpillar is a bad company — and it doesn’t mean a crash is imminent. It means that, relative to a peer set of comparable industrial and machinery businesses, the market is assigning CAT a richer-than-average valuation for its current profit profile.

In plain English: at today’s price, you’re paying a premium versus similar names. When valuation is already stretched, future shareholder returns tend to rely much more on fundamentals doing the work — ongoing earnings power, disciplined capital allocation, and dividend growth — and much less on a helpful valuation tailwind. For Caterpillar, that matters because it’s cyclical: if the cycle cools while the stock is priced at a premium, the margin for error gets thinner.

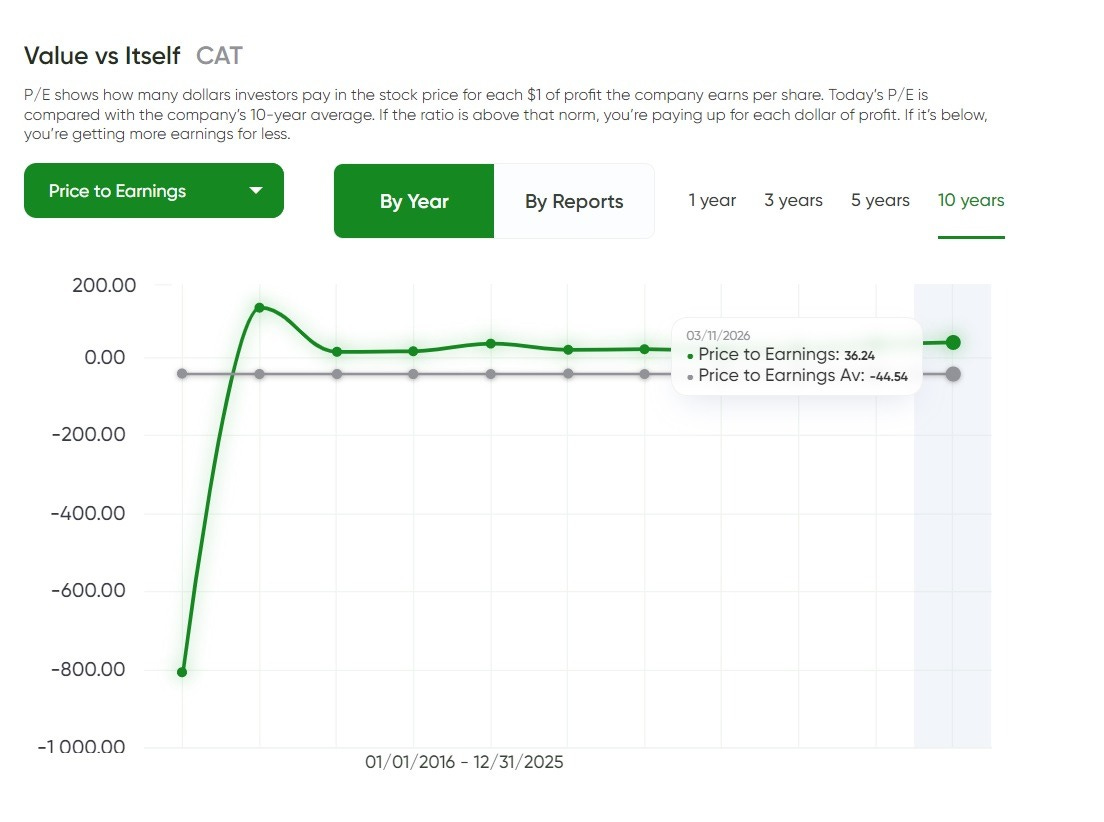

Cheaper than its own history?

⚠️ More expensive vs. its own 10-year average.

On a “value vs. itself” basis, Caterpillar (CAT) doesn’t screen as cheap versus its own history — but the comparison needs context. The current P/E is around 36.24, while the 10‑year “average” shown is around -44.54, which is a sign the average is being distorted by periods when earnings were negative (making the P/E meaningless or flipping it below zero).

In plain English, this is one of those cases where the historical P/E average isn’t a clean anchor for valuation work. When a company has loss years inside the lookback window, the “average P/E” can become mathematically misleading. For Caterpillar, that’s especially relevant because the business is cyclical and has had periods where profits compressed sharply. The practical takeaway for dividend investors is that you shouldn’t rely on this single “vs. itself” P/E comparison to conclude CAT is cheap or expensive; it’s better treated as a reminder to normalize earnings across the cycle and use multiple valuation lenses before making an income-focused entry decision.

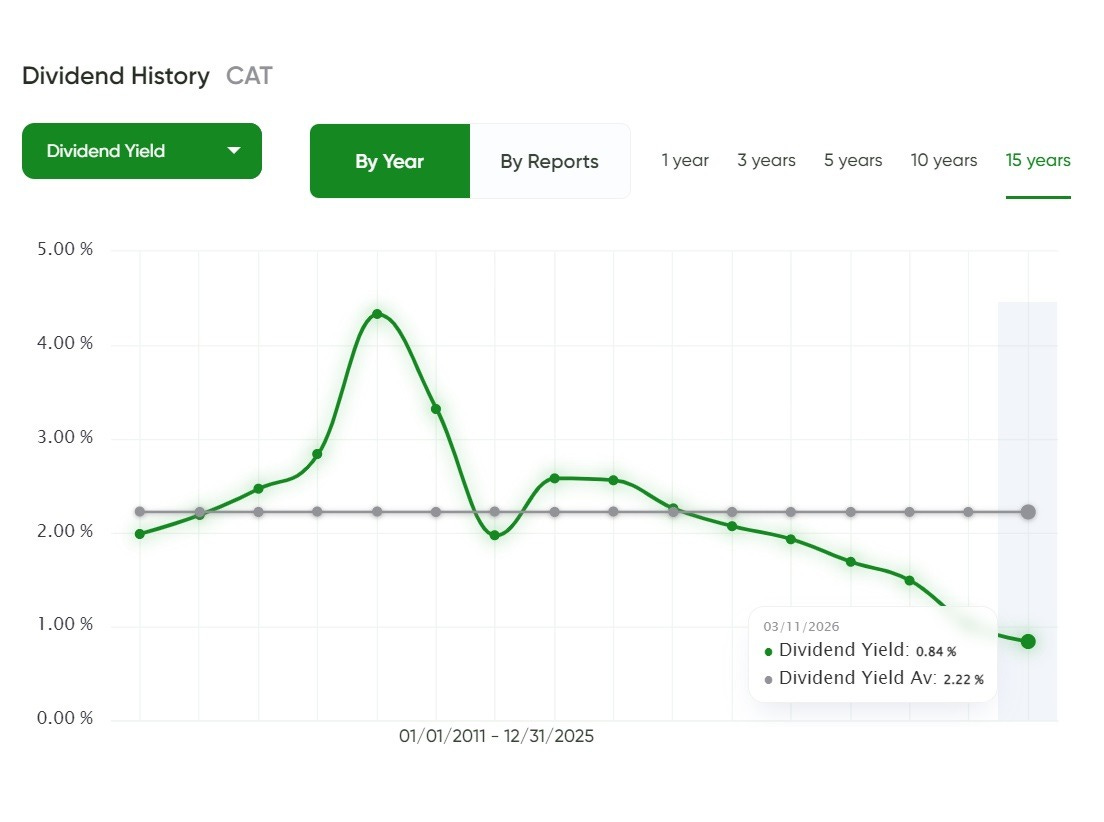

Better Yield Than Usual?

⚠️ Yield below its 10-year average.

Right now, Caterpillar (CAT) is yielding about 0.84%, while its long-term average yield over the 15-year view sits near 2.22%. That spread tells you the starting income today is well below what investors have typically received over this period, which usually happens when the share price has run ahead of dividend growth and the market is keeping the valuation firm.

In plain English, CAT is offering less income than usual versus its own history. That doesn’t make it a weak dividend stock — Caterpillar’s appeal is more about dividend growth and total-return compounding than headline yield — but it does mean you’re not getting a “historically generous” entry point on yield. For dividend investors, that shifts the decision. The case for CAT at today’s yield is less about locking in meaningful income now, and more about being comfortable with a low starting yield that can build over time through continued dividend increases, provided the cycle remains supportive and earnings stay strong enough to carry that growth.

Analyst Consensus

⚠️ Analysts don’t see meaningful short-term upside for Caterpillar (CAT).

The average 12‑month price target for Caterpillar is about $736.21, implying roughly +3.91% upside from current levels. The target range is wide — from around $425.00 on the low end to about $877.52 on the high end. Overall consensus leans Buy, based on 29 ratings, with the mix clearly tilted positive but still including a meaningful number of Holds (and a small Sell bucket).

In plain English, analysts see Caterpillar as having only modest upside over the next year, but with unusually high dispersion in outcomes — which is typical for a cyclical industrial where the macro path can dominate near-term results. For dividend investors, that’s a useful framing: the case for owning CAT isn’t about a quick “pop,” especially with today’s low starting yield. It’s about owning a high-quality, shareholder-friendly industrial through the cycle and letting returns come primarily from business execution and dividend compounding, rather than relying on a near-term re-rating.

Is This One for Me?

Here’s how Caterpillar stacks up under the MaxDividends lens:

How This Company Makes Money?

Do I clearly understand how Caterpillar (CAT) earns its money — and does the business make sense to me?

🟢 Yes: a scale-driven industrial ecosystem built on an enormous installed base, a global dealer network, and recurring aftermarket demand. Caterpillar makes money primarily by selling heavy equipment and engines into construction, mining, and energy/transport markets, then monetizing the decades-long lifecycle that follows through parts, service, rebuilds, and dealer-supported support. Earnings are shaped by end‑market activity, price and mix discipline, manufacturing efficiency, and how effectively the company captures high-margin aftermarket revenue across its fleet in the field. The result is a business that is undeniably cyclical, but still anchored in an essential, repeat-need reality: machines break, fleets age, and customers pay for uptime regardless of the market mood.

Is This a Good Stock to Buy Long Term?

Has the company shown the kind of consistency and resilience I want to see?

🟢 Yes: Caterpillar has demonstrated the kind of durability dividend investors look for, including through real-world cycle stress. The company has raised its dividend for decades, and the long-term dividend history shows the clean, upward “stair-step” profile that usually signals a payout driven by policy and discipline rather than a one-time boom.

What makes Caterpillar’s record more convincing is that this is a deeply cyclical business that has still kept the dividend moving forward through periods when end markets weakened and earnings came under pressure. Earlier in the decade-long financial picture, profitability even dipped into a loss before rebounding and building to a much higher earnings base later on. Through that kind of volatility, Caterpillar maintained its dividend posture and then strengthened coverage as results recovered. That sequence matters because it demonstrates resilience in practice — not just in theory.

Is the Stock Undervalued Today? 💵

⚠️ It looks overvalued versus peers, and the “value vs. itself” picture isn’t a clean anchor, while the current yield is well below its long-term average. In the MaxDividends app, Caterpillar screens as Overvalued relative to its peer group, which implies the market is not offering a clear “peer discount” and you’re paying up versus similar industrial names based on the current profit profile.

At the same time, CAT’s “value vs. itself” comparison on P/E is tricky to use. The current P/E sits around 36.24, but the 10‑year “average” shown is distorted by periods of negative earnings, which can make the historical average mathematically misleading rather than genuinely informative about what CAT “normally” trades at. In a cyclical business like Caterpillar, that’s a reminder to think in terms of normalized, through-the-cycle earnings rather than relying on a single long-term average multiple.

The yield picture is more straightforward and points in the opposite direction for income-focused entry timing: Caterpillar’s dividend yield is about 0.84% today versus a long-term average near 2.22%, meaning the starting income is far lower than what investors have typically received. Put differently, this is not a historically generous yield entry point.

Taken together, Caterpillar doesn’t read like a classic value-style dividend setup right now. It looks more like a high-quality dividend grower priced at a premium versus peers, with valuation signals that require cycle-aware interpretation, while the current yield is unusually low compared with its own history. For dividend investors, that can still be workable if the goal is long-run compounding and you’re comfortable paying up for quality — but it’s not the kind of entry where valuation does the heavy lifting for you.

Does It Fit Your Plan?

Dividend investing works best when each position has a job. If you treat every “dividend stock” as the same product, you end up with a portfolio that looks diversified on paper but behaves like a collection of mismatched bets. In my framework, dividend names usually fall into two buckets: anchors that deliver meaningful income from day one, and builders that start small but can grow into serious income producers as the dividend compounds.

Caterpillar (CAT) is clearly a builder, not an income anchor. The MaxRatio reading of 1.63 puts it in the Growth Eagle category, which is consistent with what you see in the yield: the current payout is modest. What you’re really buying with CAT isn’t a high coupon — it’s a long history of dividend increases and the capacity for that payout to keep climbing when the business is executing well.

The underlying logic is straightforward. Caterpillar is tied to capital spending and it will always be cyclical, but it’s not a “one-and-done equipment sale” story. The installed base of machines creates ongoing parts and service demand, and the dealer network gives CAT reach and durability that’s difficult to replicate. That ecosystem is why the company can take a hit in a downcycle, then rebuild earnings power when conditions normalize — and why the dividend has remained a priority even when the operating backdrop got rough.

So CAT tends to fit best for dividend investors who are playing the long game: people who don’t need maximum income today, can live with a cycle-driven earnings profile, and want a high-quality industrial where dividend growth and long-run compounding are the main payoff.

Final Take

Caterpillar has earned its reputation in a similar “real-economy” way: it builds the machines that move dirt, ore, and materials, and it supports those machines for decades through a dealer and service ecosystem that’s difficult to replicate. For dividend investors, the appeal isn’t a flashy yield story. It’s the combination of a long-running dividend commitment and a business that remains relevant as long as the world keeps building infrastructure, extracting resources, and maintaining industrial capacity. The dividend history reflects that culture — steady, policy-driven increases rather than opportunistic payouts that disappear when conditions tighten.

The nuance is the entry point. On a peer-relative basis, the MaxDividends App doesn’t frame Caterpillar as a bargain right now; it screens as overvalued versus its comparison set, which suggests you’re paying a premium for quality. On a “versus itself” basis, the usual P/E comparison is less helpful here because parts of the lookback period include loss or unusually weak earnings, which can distort long-term averages and make the “normal” multiple hard to pin down cleanly for a cyclical industrial. Meanwhile, the yield is the clearest signal: at roughly 0.84% today versus a long-term average near 2.22%, the starting income stream is far from historically generous.

Put together, Caterpillar still clears the quality bar as a Proven Dividend Eagle and can make sense as a long-duration dividend growth holding for investors who want industrial exposure with shareholder-friendly policy. But the current setup looks more like a “pay up for quality” situation than a classic value-style entry. If the price cools enough to lift the yield closer to its historical range — or if valuation versus peers becomes less stretched — the risk/reward profile becomes materially more attractive for conservative dividend investors.

***

The same simple formula I just used for Caterpillar works for any stock. No hype, no noise — just clear steps that let you see whether a company truly fits your plan.

And the best part? This isn’t theory. It’s all already built into the MaxDividends app: the Financial Score, the MaxRatio, the Top Dividend Eagles list, and even my own personal shortlist. Everything in one place, ready whenever you are.

MaxDividends is a treasure chest for dividend investors of any size and focus. Whether you’re after growth, balance, or pure income, you’ll find the tools and the community to back you up.

This series of case studies is here to show you just how simple — and powerful — dividend investing can be. One stock at a time, you’ll see the clarity, the confidence, and the peace of mind that comes from building your own growing stream of passive income.